Interest Rates, Futures and Seasonal Trading Patterns

|Many traders are surprised to hear that financial Futures have a Seasonal pattern. They assume agricultural or energy products do, but not so much the financial products. All markets, regardless of financial or physical, have some form of recurring cyclical pattern (Seasonal pattern) to them.

Currency markets usually exhibit a Seasonal pattern at their countries fiscal year end. Some countries will repatriate their currency or perhaps make expenditures to balance their financial statements for year end.

Interest rate markets will typically have higher yields (lower prices) coming into the April 15th tax season deadline when the government needs to raise cash to pay for tax refunds.

Stock indexes like to see sideways price action between June and September during the slow summer months when many investors are on vacation. Once back from the break the autumn season volatility starts and then we see a rally into year end. The yearend rally is usually called the Santa Claus rally.

These are just some of the typical reasons a financial product could have a reoccurring Seasonal pattern.

In this article I would like to talk about a Seasonal pattern for the futures market that Moore Research has found to be a very reliable Interest rate market strategy. I would like to thank MRCI for permission to use their content for this article.

Note: This information is not to be construed as a trade recommendation, but exclusively for educational purposes only.

I use Seasonal patterns as a market screener each month trying to identify markets that have a Seasonal catalyst to get the price moving in one direction or the other.

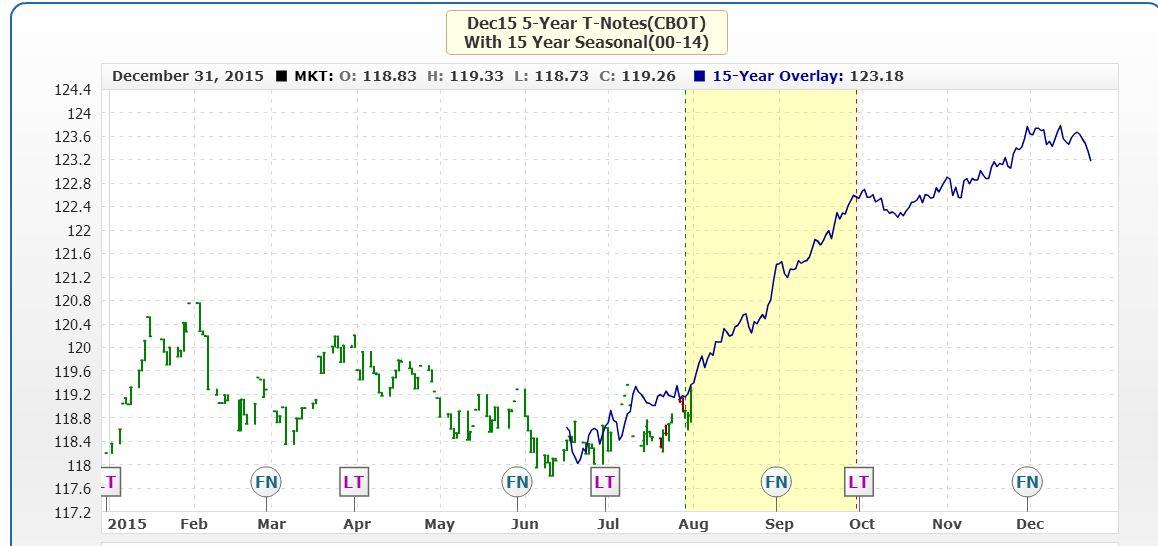

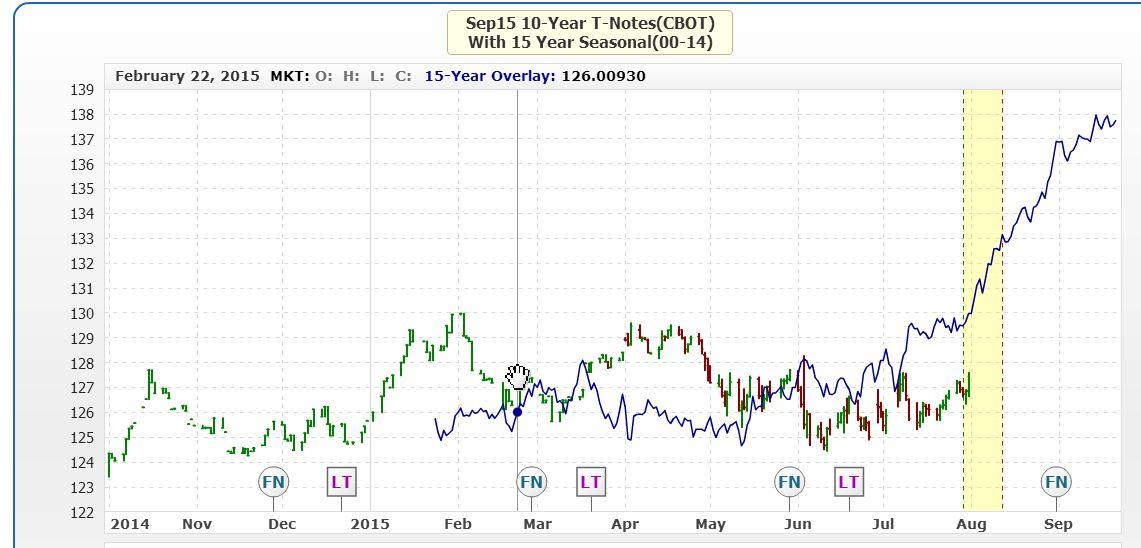

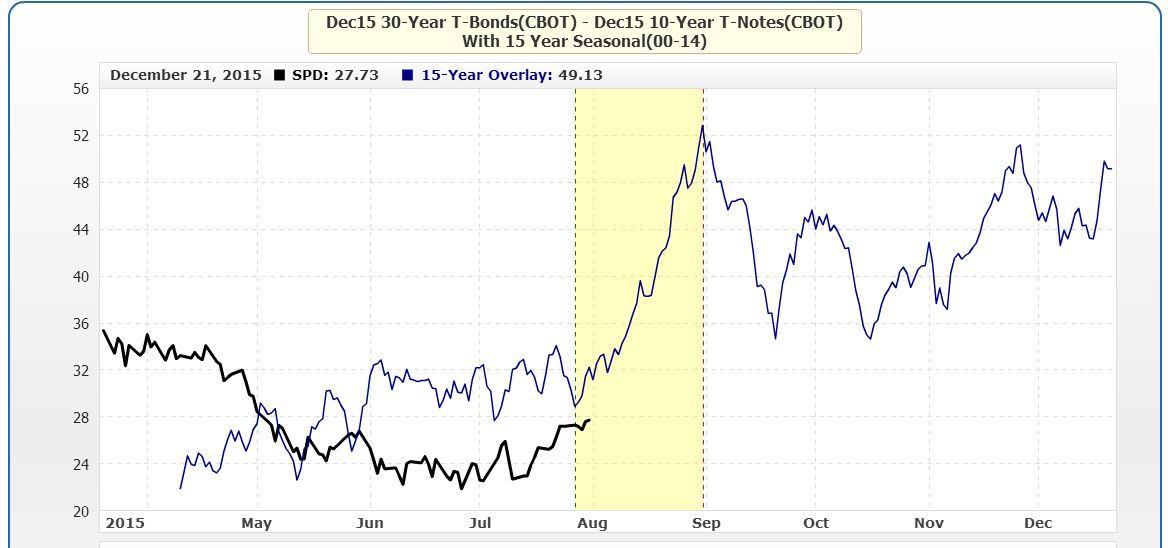

MRCI has found the 5 year Treasury (FV or ZF) has closed higher on Sept 29 than on July 29 100% of the time in the last 15 years. The 10 year Treasury (TY or ZN) has closed higher on Aug 12 than on July 29 93% of the time in the last 15 years. And for Spread traders they have found the Bonds over Notes (BON Spread) has closed higher on Aug 31 than on July 27 93% of the time as well.

MRCI and any trader who uses Seasonal patterns will tell you that a trader should “never ever” blindly buy or sell on a Seasonal date. Even the best Seasonal patterns can fail on any given year. All it takes is an event occurring this year that had not during the testing period of the prior 15 years. This could be weather, geo-political, war or any supply disruption.

A good Seasonal trade still takes analysis to time your entry using a good level. A trend in the direction of the Seasonal is very helpful as well. And of course, a written plan describing how a trader will manage the trade once in it.

Chart 1 shows the 5 year Treasury Seasonal pattern in blue. The yellow vertical box represents the optimal Seasonal window. The blue line represents the 15 year average price action of the 5 year Treasury contract.

{kind=link}

Looking at the price action coming into the Seasonal window we can see the market is heading in the right direction to confirm, so far, the Seasonal pattern this year. Even with the talk of the Federal Reserve raising interest rates in September, the price is going higher ignoring the news. Note this trade uses the December Futures contract due to the length of the trade taking you into First Notice day for the September contract. MRCI does a good job keeping a trader out of delivery situations.

Chart 2 is a chart of the 10 year Treasury Seasonal pattern.

{kind=link}

Much like Chart 1, price on the 10 year Treasury has started up coming into the Seasonal buy window. Will prices keep going higher? It is up to the individual trader to monitor their positions with protective stops and a price target if needed.

During this time of the year the government does not have to auction as many Treasuries for raising cash going into the United States fiscal year end Sept 30. Perhaps this is the reason for such a high frequency occurrence. This Seasonal pattern should have an impact all across the yield curve with the long end 30 year Treasury responding the most aggressively. The long end of the maturity curve usually acts more violently as there is more fear holding longer dated Treasuries.

The other Seasonal is the Bonds over Notes (BON) Spread. Usually a trader would enter this Spread if they feel that interest rates are going to decline. If a trader thought that rates were going to go up they would trade the Notes over Bonds (NOB) Spread. But with a probability of the BON appreciating it makes sense traders would be looking at the BON instead of NOB.

Chart 3 is a chart of the BON Spread. Unlike Charts 1 & 2 that used candle sticks, the BON chart shows a line on close chart representing where the Spread has closed each day. The dark black line represents the actual Spread this year and the blue line represents the 15 year average price pattern.

{kind=link}

A BON Spread would have a trader long December 30 year Bonds and simultaneously short the December 10 year Notes. This is referred to as an Inter-market Spread.

The interesting thing about these 3 trades is how across 2 different styles of trading, Futures and Spreads, both have a very high percentage win rate. When both of these line up it helps support the trade in some cases.

If you feel Seasonal trading might benefit your trading, MRCI still has their complimentary trial subscription. Make sure you are comfortable with technical analysis (OTA’s core strategy) before trying this.

“The year you were born marks only your entry into the world. Other years where you prove your worth, they are the ones worth celebrating.” Jarod Kintz

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers.